What to Expect from This Report MARKET STRATEGY REPORT

We’re holding a constructive outlook for both economic growth and corporate earnings in 2026. Equity markets should benefit from this fundamental strength, in our view. But there are two more reasons stocks could feel tailwinds in 2026: accommodative fiscal and monetary policy.

The Federal Reserve already resumed rate cuts in late 2025, and we think the conditions—moderating inflation, weak jobs market data—for additional cuts are becoming evident. On the fiscal side of the ledger, the One Big Beautiful Bill Act (OBBBA) is poised to deliver near term stimulus in the form of refunds/credits for both businesses and households, which lift disposable income, capex, and margins. In a midterm election year, we could also see additional fiscal stimulus to ‘juice’ the economy, and those proposals are already being floated by the Trump administration.1

In this report we’ll also address the Venezuela issue, separating Venezuela’s geopolitics from investable math, showing why sub-1% global output and slow-to-scale oil capacity argue for limited, slow-moving effects on prices and Energy earnings. Lastly, we’ll zoom out to earnings: Tech remains a powerful engine, but the setup favors broader participation in 2026, with revisions and cash-flow dynamics doing more heavy lifting than headlines.

How Fiscal + Monetary Policy Could Form a 2026 Tailwind

2026 is setting up for what we’re calling a “policy one-two”: lagged effects of Fed easing with the potential for more rate cuts on deck, combined with a visible fiscal impulse from the One Big Beautiful Bill Act (OBBBA) and additional f iscal stimulus proposals that the Trump administration seems poised to pursue.

Let’s start with monetary policy.

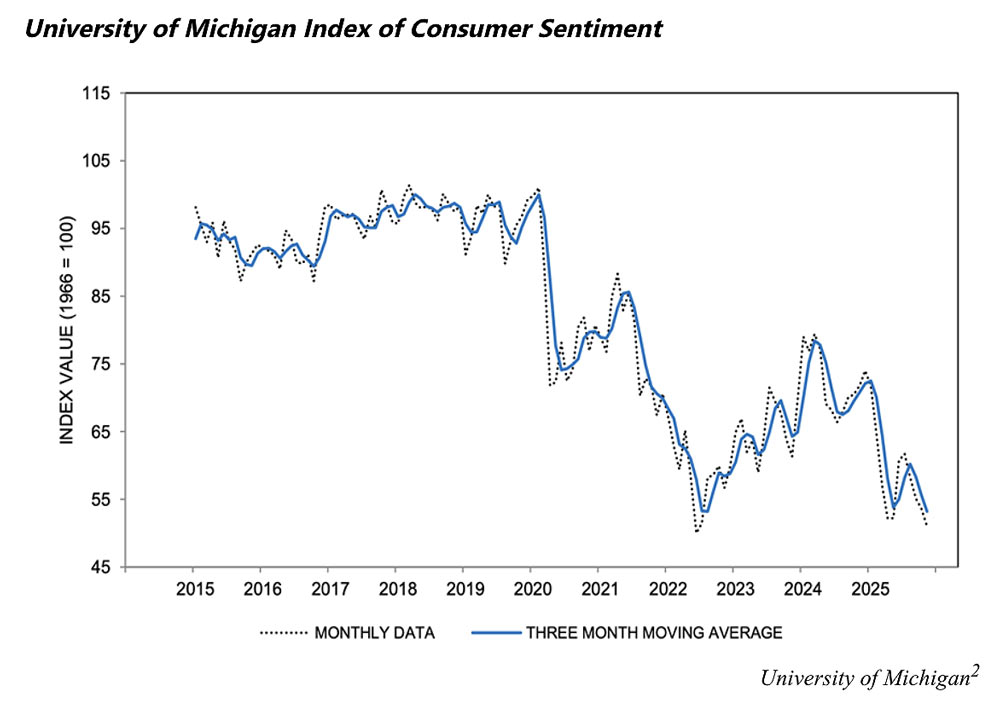

December’s employment report capped a weak year for hiring, with total job gains in 2025 averaging fewer than 50,000 per month—the slowest pace outside of recessions since the early 2000s. While the unemployment rate edged lower to 4.4% in the latest jobs report, other indicators point to softening beneath the surface. Average weekly hours declined, temporary help employment fell, and long-term unemployment rose. Job growth became increasingly concentrated in healthcare and leisure, while manufacturing employment continued to contract.

In our view (assuming inflation doesn’t reaccelerate), this should open the door for further easing in 2026. Markets broadly expect additional policy support.

The Fed has already cut rates at the last two meetings, and financial conditions have been easing. We think this will continue to serve as a positive tailwind for stocks.

On the fiscal side, the OBBBA is designed to arrive in 2026 in a way households will actually feel. Rather than mid-year paycheck withholding changes, the bill channels relief through tax filing season. Some estimates call for an aggregate 44% jump in 2026 tax refunds versus this year, roughly $150 billion flowing to consumers.

1 Wall Street Journal. January 13, 2026. https://www.wsj.com/politics/policy/in-pivot-on-affordability-trump-unveils-barrage-of-proposals-to-address-costs961e4343?mod=article_inline

DISCLAIMER

Past performance is no guarantee of future results. Inherent in any investment is the potential for loss. Zacks Investment Management, Inc. is a wholly-owned subsidiary of Zacks Investment Research.

Zacks Investment Management is an independent Registered Investment Advisory firm and acts as an investment manager for individuals and institutions. Zacks Investment Research is a provider of earnings data and other financial data to institutions and to individuals.

This material is being provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Do not act or rely upon the information and advice given in this publication without seeking the services of competent and professional legal, tax, or accounting counsel. Publication and distribution of this article is not intended to create, and the information contained herein does not constitute, an attorney-client relationship. No recommendation or advice is being given as to whether any investment or strategy is suitable for a particular investor. It should not be assumed that any investments in securities, companies, sectors or markets identified and described were or will be profitable. All information is current as of the date of herein and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole.

Any projections, targets, or estimates in this report are forward looking statements and are based on the firm’s research, analysis, and assumptions. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. All expressions of opinions are subject to change without notice. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed in this presentation.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties. Zacks Investment Management does not assume any responsibility for the accuracy or completeness of such information. Further, no third party has assumed responsibility for independently verifying the information contained herein and accordingly no such persons make any representations with respect to the accuracy, completeness or reasonableness of the information provided herein. Unless otherwise indicated, market analysis and conclusions are based upon opinions or assumptions that Zacks Investment Management considers to be reasonable. Any investment inherently involves a high degree of risk, beyond any specific risks discussed herein.

The S&P 500 Index is a well-known, unmanaged index of the prices of 500 large-company common stocks, mainly bluechip stocks, selected by Standard & Poor’s. The S&P 500 Index assumes reinvestment of dividends but does not reflect advisory fees. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index. The Russell 1000 Growth Index is a well-known, unmanaged index of the prices of 1000 large-company growth common stocks selected by Russell.

The Russell 1000 Growth Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

Nasdaq Composite Index is the market capitalization-weighted index of over 3,300 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depositary receipts, common stocks, real estate investment trusts (REITs) and tracking stocks, as well as limited partnership interests. The index includes all Nasdaqlisted stocks that are not derivatives, preferred shares, funds, exchange-traded funds (ETFs) or debenture securities. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Dow Jones Industrial Average measures the daily stock market movements of 30 U.S. publicly-traded companies listed on the NASDAQ or the New York Stock Exchange (NYSE). The 30 publicly-owned companies are considered leaders in the United States economy. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Russell 2000 Index is a well-known, unmanaged index of the prices of 2000 small-cap company common stocks, selected by Russell. The Russell 2000 Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot invest directly in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The S&P Mid Cap 400 provides investors with a benchmark for mid-sized companies. The index, which is distinct from the large-cap S&P 500, is designed to measure the performance of 400 mid-sized companies, reflecting the distinctive risk and return characteristics of this market segment.

The S&P GSCI is the first major investable commodity index. It is one of the most widely recognized benchmarks that is broad-based and production weighted to represent the global commodity market beta. The index is designed to be investable by including the most liquid commodity futures, and provides diversification with low correlations to other asset classes. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Russell 1000 Value Index is a well-known, unmanaged index of the prices of 1000 large-company value common stocks selected by Russell. The Russell 1000 Value Index assumes reinvestment of dividends but does not reflect advisory fees. An investor cannot directly invest in an index. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The Nikkei Stock Average, the Nikkei 225 is used around the globe as the premier index of Japanese stocks. More than 60 years have passed since the commencement of its calculation, which represents the history of Japanese economy after the World War II. Because of the prominent nature of the index, many financial products linked to the Nikkei 225 have been created are traded worldwide while the index has been sufficiently used as the indicator of the movement of Japanese stock markets.

The Nikkei 225 is a price-weighted equity index, which consists of 225 stocks in the 1st section of the Tokyo Stock Exchange. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor.

The CBOE Volatility Index (VIX) is a calculation designed to produce a measure of constant, 30-day expected volatility of the U.S. stock market, derived from real-time, mid-quote prices of S&P 500 Index call and put options. On a global basis, it is one of the most recognized measures of volatility — widely reported by financial media and closely followed by a variety of market participants as a daily market indicator. The volatility of the benchmark may be materially different from the individual performance obtained by a specific investor. An investor cannot invest directly in an index.